You aren’t actually “behind” on your life just because your bank account doesn’t look like a TikTok influencer’s highlight reel. It’s incredibly easy to feel paralyzed when you’re staring down undergraduate student loan interest rates of 6.52 percent while trying to find an apartment that doesn’t eat your entire paycheck. You want to build a future, but the gap between your entry-level wage and the cost of living feels like a canyon. We get it. The pressure to have it all figured out by twenty-five is real, and it’s exhausting.

The good news is that setting financial goals for your 20s doesn’t require a six-figure salary or a miserable lifestyle. This guide is your no-fluff roadmap to stop the spiral and start building momentum, even if you feel broke right now. We’re going to show you how to take total control of your bank account without sacrificing every ounce of fun. You’ll get a clear checklist of what to do first, from snagging that 5.00 percent APY in a high-yield savings account to outsmarting the debt cycle. Let’s turn that financial anxiety into a plan you can actually follow.

Key Takeaways

- Build a $1,000 “Sleep-at-Night” fund to handle emergencies without blowing your progress or your peace of mind.

- Map out realistic financial goals for your 20s that prioritize your future freedom instead of just following restrictive rules.

- Learn the hybrid approach to balance student loan payments with investing so you never miss out on a company match.

- Trade traditional, boring budgets for an “Anti-Budget” strategy that focuses on intentional spending for the things you actually love.

- Establish a simple 20-minute monthly ritual to keep your bank account in check and your momentum high.

Why Financial Goals in Your 20s Feel Impossible (And Why They Aren’t)

Your social media feed is a liar. It shows you twenty-three year olds on private jets and peers who somehow bought a house before they could legally rent a car. This constant stream of highlight reels creates a crushing sense that you’re already behind. When you’re staring at a bank balance that barely covers your groceries, setting financial goals for your 20s feels like a cruel joke. It’s easy to assume that “real” money moves are reserved for people with corporate titles and six-figure salaries. That assumption is exactly what keeps people stuck in a cycle of paycheck-to-paycheck stress.

We need to reframe how you look at your money. Most people see a budget as a cage. In reality, your goals are tools for freedom, not rules for restriction. They give you the power to say “yes” to a last-minute road trip because you aren’t terrified of your credit card statement. A financial goal is a contract with your future self. By making small moves now, you’re buying back your time and your sanity later on. Mastering basic personal finance principles doesn’t require a math degree; it just requires a shift in perspective.

The “I’m Broke” Paradox

There’s a common myth that you need to wait for a “real job” to start caring about your money. The truth is that having a smaller income makes your plan more important, not less. When margins are thin, every dollar has a bigger job to do. We know the 2026 economy isn’t doing you any favors. With undergraduate student loan interest rates at 6.52 percent and housing costs still climbing, the pressure is immense. Validating that stress is the first step toward beating it. You don’t need a massive windfall to start; you just need to decide that your current situation doesn’t define your financial ceiling.

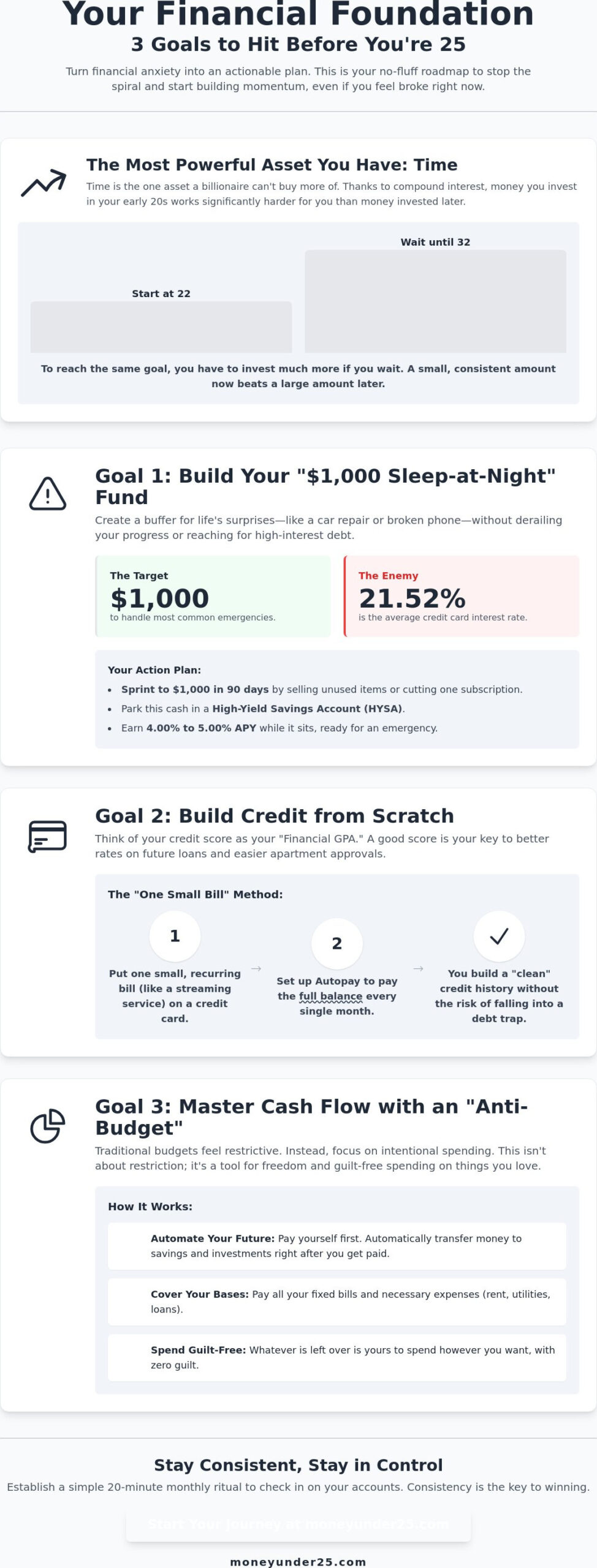

The Power of Compound Interest (The Only Math You Need)

Time is the only asset you have that a billionaire can’t buy more of. This is why $50 invested today is worth significantly more than $500 invested a decade from now. When you start at twenty-two, your money has decades to grow, multiply, and do the heavy lifting for you. If you wait until thirty-two to start, you have to work twice as hard to reach the same result. Consistency beats the actual dollar amount every single time. Even if you can only spare the cost of a few takeout meals a month, get that money moving. Achieving financial goals for your 20s is about building the habit of winning, one small deposit at a time.

The “Starter” Foundation: 3 Goals to Hit Before You’re 25

Most financial experts tell you to save six months of expenses immediately. If you’re currently checking your balance before buying a latte, that advice feels like a punch in the gut. It’s too big. It’s demoralizing. Instead of aiming for a mountain, let’s start with three entry-level financial goals for your 20s that actually feel achievable. These are your foundational moves. They aren’t about being rich yet; they’re about making sure a flat tire doesn’t ruin your entire month. Think of these as the “starter pack” for your future freedom.

The $1,000 Emergency Fund Sprint

One thousand dollars is the magic number. It’s enough to cover most “life happens” moments, like a sudden car repair or a broken phone screen. When you have this “Sleep-at-Night” fund, you stop reaching for a credit card every time something goes wrong. This is vital when the average credit card interest rate is sitting at a staggering 21.52 percent. You can scrape this together in 90 days by selling unused clothes, picking up a few extra shifts, or cutting one recurring subscription. Put this cash in a High-Yield Savings Account (HYSA). As of June 2026, top rates are between 4.00 percent and 5.00 percent APY, so your money actually grows while it sits there.

Building Credit from Scratch

Think of your credit score as your financial GPA. You don’t need a high-paying job to build it, but you do need a strategy. The “one small bill” method is the safest way to start. Put one recurring charge, like your monthly streaming service, on a credit card and set it to autopay the full balance every single month. This shows lenders you’re responsible without letting you fall into a debt trap. Following these five financial priorities helps you build a “clean” history before you ever need to apply for a car loan or an apartment lease.

Finally, you need to master your cash flow. This isn’t about living like a monk or never eating out again. It is simply knowing exactly where your money goes before the month even starts. When you understand your inflow and outflow, you stop wondering where your paycheck disappeared to. If you’re ready to get serious about these basics, checking out tools for effective finance management can help you stay on track without the headache. These three goals are the entry-level versions of the big wealth-building moves we’ll cover next. Once you hit these, the “I’m behind” feeling starts to fade away.

The Great Debate: Paying Off Debt vs. Starting to Invest

It’s the question that keeps every twenty-something awake at 2:00 AM: “How am I supposed to invest for the future when I still owe $30,000 in student loans?” It feels like you’re trying to fill a bucket that has a giant hole in the bottom. Many traditional advisors suggest paying off every cent of debt before you even look at a stock. We disagree. This all-or-nothing approach ignores the reality of how wealth actually grows. When you’re setting financial goals for your 20s, the smartest move is often a hybrid approach that tackles debt while letting your future money start cooking.

The first rule is to categorize your debt by its danger level. High-interest debt, like a credit card with a 21.52 percent APR, is a financial emergency. It’s a house on fire that needs to be put out immediately. On the other hand, undergraduate student loans at 6.52 percent are more like a slow leak. While you’re paying those down, you shouldn’t ignore your employer’s 401(k) match if they offer one. Ignoring your 401(k) match is like turning down a raise. It’s literally free money that your future self is counting on. You can contribute enough to get the match while still aggressively attacking your high-interest balances.

The “Debt Avalanche” vs. “Debt Snowball”

When it comes to paying off those balances, you have to pick a strategy that matches your personality. The Debt Avalanche method is for the math lovers; you pay off the debt with the highest interest rate first to save the most money over time. The Debt Snowball method is for the win seekers. You pay off the smallest balance first to get a quick psychological victory. If you need to see progress to stay motivated, go with the snowball. If you want the most efficient path, go with the avalanche. Both are valid financial goals for your 20s as long as they keep you moving forward.

Investing for Beginners (Start With $5)

You don’t need a massive portfolio to be an investor. Thanks to micro-investing apps and fractional shares, you can start with the change from your morning coffee. The “Set it and Forget it” goal is simple: automate a $20 investment every month. At this stage, the habit of investing is far more valuable than the initial profit you see on the screen. You’re training your brain to see yourself as an owner, not just a consumer. By the time you reach your 30s, you’ll have the systems in place to scale your wealth without even thinking about it.

Beyond the Bank Account: Career and Lifestyle Goals

Your 20s are the ultimate time to take calculated career risks. You don’t have a mortgage yet. You probably don’t have kids relying on your every move. This is your window to bet on yourself. Building wealth isn’t just about how much you save; it’s about how much you can eventually earn. When you look at financial goals for your 20s, you have to look past the spreadsheets and into your daily habits. If you only focus on cutting back, you’ll eventually hit a wall. If you focus on growing your value, your potential is limitless.

Investing in Your Earning Power

Sometimes, spending money is the fastest way to make more of it. A $500 specialized certification can be worth significantly more than keeping that same $5,000 in a savings account. Why? Because that certificate might jumpstart a $15,000 salary increase. This is called skill-stacking. You’re layering new abilities on top of your existing ones to become irreplaceable. Don’t forget that networking is a financial asset, too. Even for introverts, building a circle of “people who know what you’re capable of” is the best insurance policy against a bad economy. Use a side hustle as a learning lab. It’s not just a paycheck; it’s a way to test new skills without risking your main income.

Values-Based Spending (Stop Buying Things You Hate)

The “Latte Factor” is a lie. Skipping a $6 coffee won’t make you a millionaire if you’re overpaying for a car you don’t need or an apartment that eats 50 percent of your income. Focus on the big wins: rent, transportation, and food. This is the “Anti-Budget” approach. You decide what you value most and cut costs ruthlessly on everything else. If you love travel, spend there. If you don’t care about designer clothes, stop buying them just to fit in. You’ll find it’s much easier to say “no” to expensive social outings when you have a specific goal in mind. Create a “Fun Fund” so you don’t burn out. If you’re tired of feeling like your money is controlling you, it’s time to start a plan for proactive finance management today.

The final piece of this puzzle is the “F* You” Fund. This is the ultimate career insurance. It’s a specific stash of cash that gives you the power to walk away from a toxic boss or a soul-crushing job without fear. When you have three to six months of bare-bones expenses saved up, you’re no longer a hostage to a paycheck. This freedom is one of the most important financial goals for your 20s because it allows you to choose your path based on growth rather than desperation. It’s the difference between being stuck and being in control.

Your One-Page Financial Roadmap for 2026

You have the theory. Now you need the execution. We’ve covered the six essential financial goals for your 20s: building that $1,000 starter fund, mastering your cash flow, cleaning up your credit, stacking skills to raise your earning ceiling, spending intentionally, and finally, funding your freedom with a “F* You” stash. It sounds like a lot when you see it all at once. Wealth isn’t built in a weekend. It’s built in those small, boring moments when you choose your future self over a temporary impulse.

To keep this momentum alive, you need a simple system. Enter the “Monthly Money Date.” Set a recurring 20-minute calendar invite for the first of every month. Grab a coffee, open your banking apps, and check your progress. Are your automated transfers still running? Did you hit your savings target? This isn’t about shaming yourself for a late-night pizza run. It’s about staying conscious of your trajectory. If you’re off track, you just pivot and keep moving. Perfection is the enemy of progress; consistency is the only thing that actually moves the needle.

The 30-Day Action Plan

Stop waiting for the “perfect” time to start. Use this checklist to kick off your new financial life over the next four weeks:

- Week 1: Track every single penny you spend. Don’t judge yourself or change your habits yet. You can’t fix what you haven’t measured.

- Week 2: Set up your High-Yield Savings Account. Automate a transfer of just $10. Proving to yourself that you can save is more important than the initial dollar amount.

- Week 3: Check your credit score. Look for errors and make sure you know exactly where you stand. Knowledge is power, even if the number isn’t where you want it yet.

- Week 4: Identify one “skill-stacking” opportunity. Find a certification or a free course that directly increases your value in the job market.

How Money Under 25 Keeps You Moving

You don’t have to figure this out alone. We created Money Under 25 to be the guide we wish we had when we were starting out. Our “no-boredom” guides break down complex topics into language that actually makes sense for your life. We’re here to help you hit those financial goals for your 20s without the dry, corporate lecture. Use our free budgeting tools and trackers to see your progress in real time. If you mess up one week, don’t throw away the whole plan. Just start again tomorrow. Ready to master your money? Check out our Finance Management tools! and let’s get to work.

Stop Wishing and Start Building Your Future

You have the roadmap; now it’s time to put the car in drive. Building wealth isn’t about having a perfect bank account on day one. It’s about deciding that you’re done with the “I’m behind” narrative and ready to take control of your own story. Whether you’re starting with your first $1,000 or finally automating a small monthly investment, these wins compound into massive freedom. Setting financial goals for your 20s is the best gift you can give your future self.

Simon David built this platform because he knew the standard education system wasn’t teaching us the skills we actually need to survive. We offer practical tools designed for $0 starting balances and no-fluff, jargon-free education that respects your reality. You don’t need a finance degree to win; you just need to start. Start Managing Your Money Like a Pro (For Free) and take the first step toward a life where you aren’t stressed about every swipe of your card. You’ve got this. Your future self is already thanking you for starting today.

Common Questions About Your Money

What are the top 3 financial goals for a 20-year-old?

The most important goals are building a $1,000 starter emergency fund, tracking your cash flow, and establishing a credit history. These three moves create a safety net that prevents you from leaning on high-interest credit cards when life gets messy. Instead of worrying about complex stock portfolios, focus on these foundational habits. They give you the control you need to handle bigger moves later in your decade.

How much money should I have saved by 25?

There is no magic number that fits everyone, but aiming for three months of bare-bones living expenses is a solid benchmark. If you’re starting at zero, don’t let that “perfect” number paralyze you. The real goal is to have enough cash to handle a sudden job change or a car repair without panic. Every hundred dollars you add to your high-yield savings account puts you ahead of where you were yesterday.

Should I save for an emergency or pay off student loans first?

Build your $1,000 “Sleep-at-Night” fund before you do anything else. Once that’s in place, focus on any high-interest debt like credit cards with 21.52 percent APRs. After the high-interest fire is out, you can balance saving more for emergencies while making your regular payments on student loans, which sit around 6.52 percent for 2026. This hybrid approach keeps you protected while you chip away at the balance.

Can I start investing with only $10 or $20 a month?

Yes, you can absolutely start small thanks to fractional shares and micro-investing apps. When setting financial goals for your 20s, the habit of investing is actually more valuable than the initial profit you see. Automating just $20 a month trains your brain to prioritize your future self. Over time, that consistency builds wealth much more effectively than waiting until you have a “large” amount to start.

Is it possible to build a good credit score without a credit card?

You can build credit by being added as an authorized user on a parent’s account or by using services that report your rent and utility payments. However, the most direct path is often the “one small bill” method using a credit card you pay off in full every month. This shows lenders you’re responsible without letting you fall into a debt trap. It’s about playing the system to your advantage.

What is a “High-Yield Savings Account” and do I really need one?

A High-Yield Savings Account (HYSA) is a bank account that pays a much higher interest rate than a standard checking or savings account. With June 2026 rates between 4.00 percent and 5.00 percent APY, you definitely need one for your emergency fund. It’s the easiest way to make your money work for you while it sits there. It keeps your cash accessible but ensures it isn’t losing value to inflation.

How do I stop feeling guilty about spending money on things I enjoy?

Adopt an “Anti-Budget” or values-based spending plan where you automate your savings and bills first. Once your future is taken care of and your obligations are met, the money left over is yours to spend guilt-free. This shift in financial goals for your 20s allows you to enjoy that concert or dinner out because you know the math already works. You’re spending with intention rather than crossing your fingers.

What should I do if I’m 25 and have $0 in savings?

Start your 30-day action plan today and stop looking in the rearview mirror. Your first move is to track every penny for one week to see where your money is actually going. You’ll likely find a few “leaks” that can be redirected into your first $100 of savings. Being 25 with nothing saved is a common starting point; the only mistake is waiting until you’re 26 to do something about it.

Pingback: How to Get $1,000 Fast (Real Methods That Work) | MoneyUnder25

Pingback: How to Pay Off Student Loans Fast (7 Strategies) | MoneyUnder25

Pingback: Emergency Fund for Beginners: How Much You Need and How to Start

Pingback: How to Negotiate Your Salary at 22 (First Job Guide)